Why Bangalore is India’s #1 City for NRI Real Estate Investment in 2026

Every major Indian city has a version of the real estate pitch. Mumbai leads with legacy and liquidity. Hyderabad leads with affordability and emerging infrastructure. Pune leads with IT corridor diversification. Bangalore’s pitch is different. It’s backed by a data density that the others can’t match, on the combination of variables that determine long-term investment performance: employment depth, appreciation consistency, rental yield strength, and infrastructure investment pipeline.

This guide makes the case for real estate investment in Bangalore in 2026 through the numbers rather than the narrative. It covers the IT economy that anchors demand, the appreciation trajectory that has defined the last six years, how Bangalore’s rental yields compare against competing metros, where NRI capital is concentrating, and what the infrastructure pipeline means for forward appreciation, with specific focus on Sarjapur Road as the corridor where these variables converge most powerfully.

TL;DR

- Bangalore led India in Q1 2026 office leasing with a 24.8% share of national volumes; GCCs accounted for the dominant share of leasing activity, per JLL.

- Sarjapur Road apartment prices have appreciated from approximately ₹5,000 per sq ft in 2020 to ₹11,000 – ₹12,000 in 2026, over 100% in six years.

- Bangalore’s gross rental yield of 3.5 – 5.5% outperforms Mumbai (1.5 – 3.0%) and is competitive with Hyderabad (2.5 – 4.0%) at a lower entry barrier.

- Luxury residential properties above ₹1.5 crore captured 53% of new launches in Q1 2026, per Anarock — a structural shift toward premiumisation.

- The best city to invest in real estate in India for risk-adjusted NRI returns in 2026 is Bangalore, driven by employment depth, yield consistency, and confirmed infrastructure catalysts

- Metro Phase 3A (Hebbal–Sarjapur Red Line), PRR Phase 1 tendering, and SWIFT City are the three infrastructure catalysts that will define Sarjapur Road’s next appreciation cycle

Bangalore’s IT Economy and Population Growth

The foundation of any real estate investment in Bangalore thesis is the employment base, specifically the depth, diversity, and growth trajectory of the technology sector that drives residential demand.

Bangalore accounts for approximately 35 – 40% of India’s total IT exports and hosts the highest concentration of Global Capability Centres (GCCs) in the country. In Q1 2026, the city recorded gross office leasing of approximately 5.3 million sq ft, a 52% increase year-on-year, with GCCs and flex space accounting for the dominant share of absorption, per JLL data. Bangalore led all Indian cities with a 24.8% share of national leasing volumes in this period.

Why employment depth matters for real estate investors:

- A city anchored to a single sector or a small number of employers is exposed to demand shocks if hiring slows. Bangalore’s IT employment spans MNCs, product companies, GCCs, startups, and fintech firms across multiple ORR corridors, which provides demand diversification that no other Indian city matches at the same scale

- The correlation between commercial office absorption and residential rental demand is direct and documented. When GCCs expand leasing, senior professionals relocate to Bangalore, creating rental demand in the ₹40,000–₹80,000 per month segment that sustains yield for premium apartment investors

- Population inflow into Bangalore has been consistently topping among tier-1 cities over the last decade. The resulting housing demand runs structurally ahead of supply in the premium segment, maintaining price floors even during broader market softening

The RBI’s cumulative 125 basis point reduction in the repo rate since February 2025 has further eased home loan conditions — NRIs can access financing with LTV ratios of up to 80% at meaningfully lower rates than two years ago.

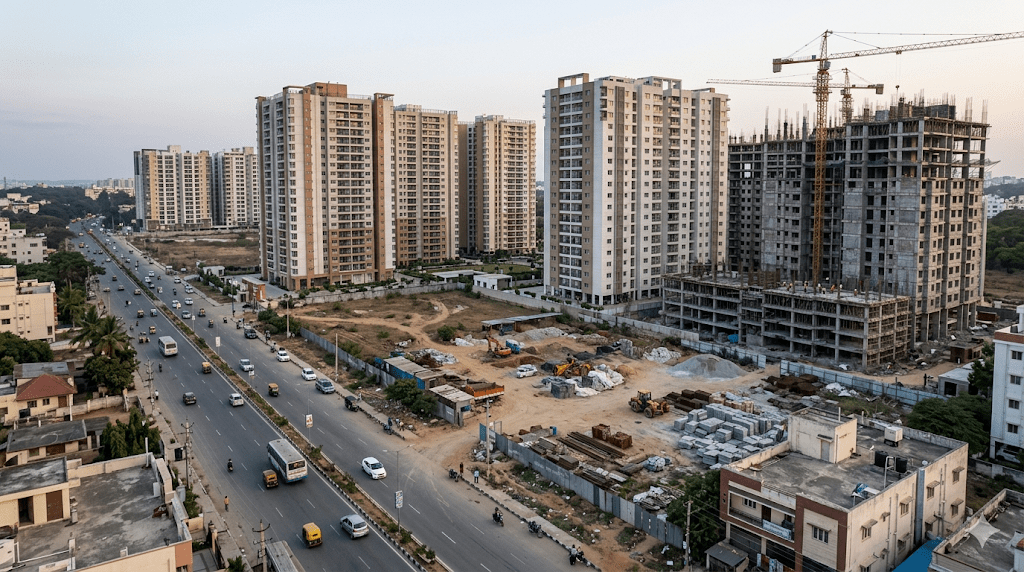

Year-on-Year Apartment Appreciation: 2020–2026

The six-year appreciation trajectory on Sarjapur Road is one of the most consistently documented appreciation stories in Indian residential real estate:

| Year | Avg. Price (₹/sq ft) | Cumulative Growth | Primary Catalyst |

| 2020 | ₹5,000 | Baseline | ORR tech expansion begins |

| 2021 | ₹6,050 | +21% | Post-pandemic demand for larger homes |

| 2022 | ₹6,900 | +38% | Infrastructure announcements; steady end-user demand |

| 2023 | ₹7,500 | +50% | Luxury segment acceleration |

| 2024 | ₹9,300 | +86% | Metro Phase 3A planning; GCC leasing surge |

| 2026 | ₹10,000–₹11,000 | +100%–+120% | SWIFT City inauguration; Infosys SEZ; premium launches |

The appreciation pattern is not uniform across Bangalore. The western corridor (Whitefield) has matured with prices ranging from ₹11,000 to ₹14,000 per sq ft, leaving limited near-term headroom. Electronic City remains a value zone at ₹7,426 per sq ft but lacks the lifestyle infrastructure to sustain premium rental demand. Sarjapur Road sits at the inflection point. Its prices have risen significantly, but the infrastructure premium (Metro Phase 3A, PRR, SWIFT City) has not yet fully materialised, meaning the appreciation runway ahead is meaningfully longer than in mature zones.

Knight Frank data indicates that the premium and luxury segment (properties above ₹1.5 crore) has maintained 14% year-on-year growth momentum, while the sub-₹1 crore segment has moderated. This is a structural shift that favours mid-premium to luxury investors over affordable-segment buyers.

Rental Yield Comparison: Bangalore vs. Competing Metros

For NRI investment in Bangalore specifically, rental yield is the near-term return while capital appreciation plays out over the holding horizon. The comparison against competing metros is one of Bangalore’s strongest arguments:

| City | Avg. Price (₹/sq ft) | Gross Rental Yield | Capital Appreciation (Annual) | Investor Profile |

| Bangalore | ₹9,500–₹12,500 | 3.5%–5.5% (6–9% luxury) | 8%–12% | Growth + yield balance |

| Mumbai | ₹20,000–₹35,000+ | 1.5%–3.0% | 5%–7% | Legacy; low yield, high lock-in |

| Hyderabad | ₹7,000–₹10,000 | 2.5%–4.0% | 6%–10% | Emerging; rental market maturing |

| Pune | ₹7,500–₹11,000 | 3.0%–4.0% | 5%–8% | IT + auto; location-sensitive |

What the yield table reveals:

Mumbai’s entry prices are prohibitive for most NRI investors outside the ultra-HNI segment, and the yield barely covers financing costs. Hyderabad offers appreciating values, but the rental market hasn’t yet deepened to the point where professional tenant pools sustain a consistent yield. Pune is stable but lacks the employment concentration depth that makes Bangalore’s demand structural rather than cyclical.

Bangalore’s 3.5–5.5% gross yield sits at a price point that remains accessible in the ₹1.5–₹2.5 crore range, and in the luxury segment on Sarjapur Road, where premium wellness apartments with amenity access command ₹40,000–₹80,000 per month in rent, yields move toward the 6–9% range. For an NRI investing in Bangalore, this combination of accessible entry, strong yield, and above-average appreciation is the core risk-adjusted case.

NRI Demand Surge: What Post-2022 Data Shows

NRI participation in Indian residential real estate has accelerated materially since 2022, driven by three converging factors:

Exchange rate leverage: The Indian Rupee has depreciated approximately 114% against the US Dollar between 2011 and 2026. For an NRI earning in USD, AED, or GBP, this means Indian premium real estate is structurally cheaper in real purchasing power terms than it was a decade ago. A property priced at ₹2 crore today costs a US-based NRI approximately USD 210,000, significantly less in dollar terms than an equivalent asset cost five years ago.

Premiumisation of supply: Luxury properties above ₹1.5 crore captured 53% of new residential launches in Q1 2026, per Anarock. Tier-1 developers like Prestige, Sobha, Godrej, and Birla have concentrated new supply in the premium segment, which is exactly where NRI capital is most active. The alignment between the supply mix and the NRI demand profile has deepened the market.

Regulatory simplification: The 2026-27 Union Budget removed the TAN requirement for NRI property transactions, replacing it with a PAN-based TDS system. The introduction of the Income Tax Act, 2025, specifically Section 393(2), which replaces Section 195 of the 1961 Act, has further simplified the TDS deduction framework for NRI sellers. Together, these changes have reduced the administrative friction that once made remote transactions feel prohibitively complex.

NRI buyers are increasingly concentrating in Bangalore’s eastern and southeastern corridors — Sarjapur Road, Whitefield, and Bellandur. Here, the combination of IT employment proximity, school ecosystem, and infrastructure pipeline aligns with both investment return requirements and eventual relocation intent.

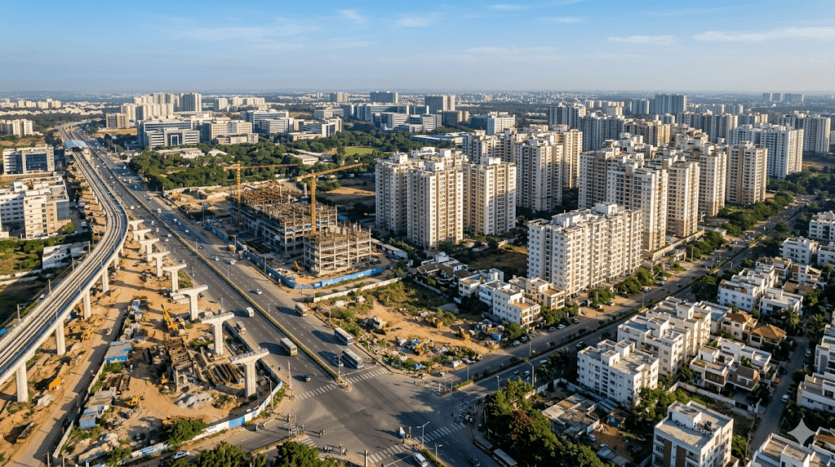

Why Sarjapur Road Is Bangalore’s Fastest-Growing Investment Zone

Within Bangalore’s residential market, Sarjapur Road is the micro-market where the investment variables converge most clearly in 2026.

The employment anchor

Wipro’s corporate campus sits directly on Sarjapur Road at Sompura Gate. RMZ Ecoworld, Ecospace, and the broader ORR tech belt are accessible from the western end of the corridor. Embassy Tech Village and the Electronic City Infosys campus are reachable via Dommasandra. This multi-employer catchment means rental demand doesn’t collapse if a single company downsizes, a structural diversification that single-anchor corridors like Electronic City cannot match.

The school ecosystem

Oakridge International, Indus International, Greenwood High, TISB, and NPS East together create the densest international school concentration in Bangalore. For NRI families planning eventual relocation, school proximity to this belt is a primary purchase driver, one that sustains residential demand independent of IT sector fluctuations.

The appreciation runway: At ₹11,000–₹14,000 per sq ft on average in 2026, Sarjapur Road has not yet reached Whitefield’s price ceiling. The eastern sub-zones of Carmelaram and Dommasandra have even more headroom. The infrastructure catalysts that will drive the next appreciation cycle are confirmed but not yet delivered, meaning buyers in 2026 are entering ahead of the premium rather than after it.

Suyug’s projects at Sompura Gate, both IGBC Silver pre-certified, RERA approved, with no shared walls, sit within this corridor at price points (starting ₹1.5 crore) that represent genuine mid-premium entry into a zone with documented long-term appreciation fundamentals.

The Infrastructure Pipeline: Metro, ORR, and PRR

Infrastructure is the forward-looking variable that separates corridors with sustained appreciation from those that plateau. Sarjapur Road’s pipeline is among the most active in Bangalore:

Metro Phase 3A — Hebbal–Sarjapur Red Line

The proposed 36-kilometre, 28-station line connects Sarjapur Road to Hebbal in North Bangalore via key interchanges at Iblur (Blue Line), Agara (Blue Line), Dairy Circle (Pink Line), and KR Circle (Purple Line).

– The DPR was optimised in October 2025 at ₹28,405 crore.

– Union Cabinet approval is anticipated in late 2026 or early 2027

– Construction 2029–2031

– Realistic operational window 2031–2033.

Historical Bangalore pattern: micro-markets see 15–25% appreciation in the 18–24 months before a metro line commissions.

Peripheral Ring Road (PRR / Bangalore Business Corridor)

Phase 1 tendering began in 2026. The 73-km expressway connects Tumakuru Road to Hosur Road, bypassing the city core for inter-zone travel and reducing Sarjapur-to-North-Bangalore travel time by up to 50% when operational.

SWIFT City and Infosys SEZ: The 1,000-acre KIADB SWIFT City on the Sarjapur-Attibele axis is projected to create over 100,000 technology and industrial jobs [VERIFY: current SWIFT City status and projections]. Combined with the 202-acre Infosys IT SEZ, this represents the next wave of employment creation that will sustain residential rental demand in the eastern corridor through the next decade.

STRR (Satellite Town Ring Road): Operational in phases from 2027, the STRR diverts heavy freight away from Sarjapur Road — directly addressing the dust and congestion concerns that residents and online forums consistently raise as liveability negatives [VERIFY: current STRR operational status].

City-by-City NRI Investment Scorecard*

| Parameter | Bangalore | Mumbai | Hyderabad | Pune |

| Avg.Entry Price (₹/sq ft) | ₹9,500–₹12,500 | ₹20,000–₹35,000+ | ₹7,000–₹10,000 | ₹7,500–₹11,000 |

| Gross Rental Yield | 3.5%–5.5% | 1.5%–3.0% | 2.5%–4.0% | 3.0%–4.0% |

| Annual Appreciation | 8%–12% | 5%–7% | 6%–10% | 5%–8% |

| Metro Connectivity | Expanding (Phase 3A) | Established | Expanding | Limited |

| School Ecosystem | Very High | High | Moderate | Moderate |

| NRI Liquidity | High | High | Moderate | Moderate |

| Entry Accessibility | Moderate | Very Low | Moderate | Moderate |

| Overall NRI Score | ⭐⭐⭐⭐⭐ | ⭐⭐⭐ | ⭐⭐⭐⭐ | ⭐⭐⭐ |

**Data sources: Compiled from Anarock, PropTiger, & JLL Q1 2026 Micro-market Indices

The scorecard reflects a consistent finding: Bangalore offers the strongest combination of yield, appreciation, entry accessibility, and employment depth among India’s tier-1 investment cities. Mumbai wins on liquidity and legacy but loses on yield and entry cost. Hyderabad is a credible secondary option, but lacks the employment diversity and school infrastructure density that make Bangalore’s residential demand structural. Pune is stable but plays a supporting role to Bangalore’s primary positioning for most NRI investors.

Sarjapur Road is where Bangalore’s NRI investment is concentrating, and for a good reason. See Suyug’s upcoming homes on the corridor, built for investors who want verified fundamentals, IGBC certification, and a long-term asset that works without active management.

One Thing Worth Sitting With

The data on real estate investment in Bangalore is clear and consistent across every credible source. What separates investors who benefit from it and those who don’t isn’t access to the data; it’s the decision to act on it before the infrastructure premium is fully priced in. In a market where Metro Phase 3A, PRR, and SWIFT City are confirmed but not yet delivered, 2026 is still inside that window.

FAQ’s :

Bangalore leads on the combination of variables that determine long-term NRI investment performance: employment depth (the highest GCC concentration in India), gross rental yield (3.5–5.5%, above Mumbai’s 1.5–3.0%), annual appreciation (8–12% in premium corridors), and an accessible entry price relative to Mumbai. The city’s IT employment base is diversified across sectors and employers, making demand structural rather than dependent on any single company or industry cycle.

Gross rental yields across Bangalore’s established IT corridors run 3.5–5.5% annually. In premium wellness developments on Sarjapur Road, which are larger configurations with full amenity access, the yields move toward 6–9%. The yield differential between standard and premium configurations reflects the depth of the senior IT professional tenant pool, which pays ₹40,000–₹80,000 per month for well-maintained, amenity-rich apartments within commuting distance of major employment nodes.

Sarjapur Road has delivered approximately 100–120% absolute appreciation between 2020 and 2026, outperforming Whitefield (which has matured at higher price points with less remaining headroom) and Electronic City (which offers lower entry prices but thinner lifestyle infrastructure). The eastern sub-zones of Carmelaram and Dommasandra have additional headroom given their confirmed Metro Phase 3A proximity at prices that haven’t yet fully priced in the infrastructure premium.

Three confirmed catalysts: Metro Phase 3A (Hebbal–Sarjapur Red Line, projected operational 2031–2033), the Peripheral Ring Road Phase 1 (tendering began 2026; reduces inter-zone travel time by up to 50%), and SWIFT City (1,000-acre KIADB development projected to create 100,000+ jobs on the Sarjapur-Attibele axis). The historical Bangalore pattern: micro-markets see 15–25% appreciation in the 18–24 months before a metro commission, so buyers entering in 2026 are approximately 6–7 years ahead of that window.

Yes, every under-construction project must be registered with Karnataka RERA (rera.karnataka.gov.in), which provides statutory protection on completion timelines, plan deviations, and possession commitments. NRI buyers should verify RERA registration tower-wise (not just project-level), check the registered completion date, and review the complaints section for unresolved buyer disputes before booking. RERA significantly reduces the project delivery risk that once made remote NRI purchases feel risky.

Bangalore’s premium residential market has delivered 8–12% annual appreciation in established corridors, outpacing the average 4–5% annual rupee depreciation against major global currencies, meaning real returns in foreign currency terms remain positive. Against US index funds or Singapore REITs, Indian premium real estate carries more liquidity risk but offers yield, appreciation, and eventual personal utility (return-to-India option value) that purely financial instruments don’t. For NRIs who intend to maintain a connection to India, the asset class offers a uniquely multi-dimensional return profile.