Real Estate Investment Myths in India: 7 Things NRIs Get Wrong in 2026

Most NRIs who haven’t invested in Indian property aren’t indifferent to the opportunity. They’re hesitant, held back by a set of concerns that were legitimate a decade ago, circulated widely enough that they’ve become received wisdom, and rarely examined against the actual regulatory and market reality existing today.

The Indian real estate landscape in 2026 is materially different from the one that generated these fears. RERA has changed the legal architecture. FEMA has always provided clearer repatriation pathways than most buyers realise. And Bangalore’s premium IT corridors have delivered consistent double-digit appreciation, changing the returns conversation entirely.

This guide goes through the seven most persistent real estate investment myths in India that hold NRI buyers back, from what the concern is, where it came from, to what the current data and regulatory framework actually show.

TL;DR

- NRIs can complete an entire property transaction remotely via a registered Power of Attorney, with no India visit required

- RERA has fundamentally changed developer accountability; escrow requirements, complaint mechanisms, and penalty structures are now statutory

- Sarjapur Road has delivered ~85%+ appreciation between 2021 and 2025, outpacing rupee depreciation and most global fixed-income alternatives.

- Professional property management platforms make remote ownership genuinely hands-off

- Premium IGBC-certified apartments in Bangalore’s IT corridors are accessible from ₹1.5 crore, and are not exclusively in HNI territory

- NRIs can repatriate up to USD 1 million per financial year from property sales under FEMA.

- Long-term capital gains tax is 12.5% flat; strategic tools like Form 128 and Section 54 exemptions reduce effective tax further.

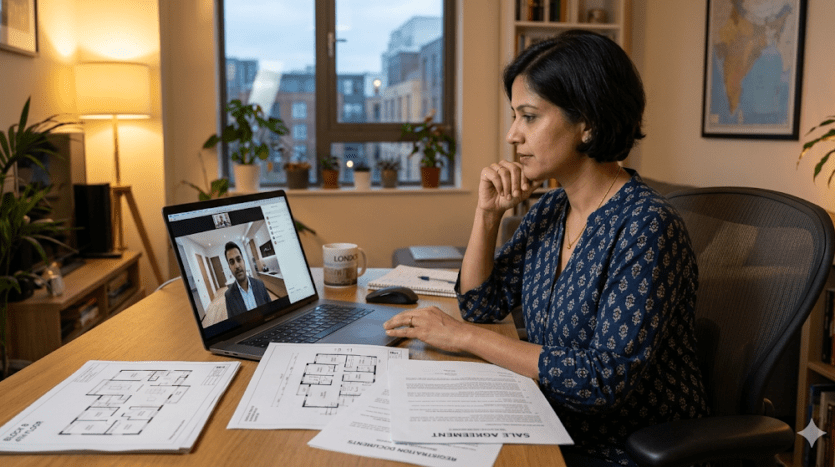

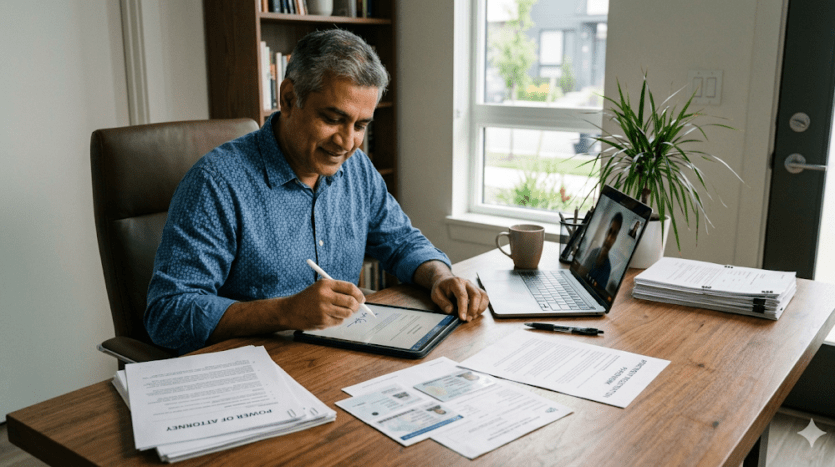

Myth 1: NRIs Can’t Buy Property Without Visiting India

The myth: Buying property in India requires being physically present for site visits, document signing, and registration, making remote transactions impractical or impossible.

The reality:

A complete property transaction can be executed from abroad without a single visit to India, provided the legal infrastructure is correctly set up. The mechanism is a registered Power of Attorney (POA) — a document that authorises a trusted representative in India to act on your behalf for a specific, defined transaction.

What the process looks like in practice:

- Execute a transaction-specific POA, limited to the particular property and set of actions rather than a general POA that carries broader risk

- Have the POA attested at your nearest Indian Embassy or Consulate in your country of residence

- Have it adjudicated at the relevant Sub-Registrar’s office within 90 days of its arrival in India, before it is used

- Your POA holder signs the sale agreement, completes registration, and handles possession paperwork on your behalf

- Further, your representative can digitally upload these documents to Karnataka’s Kaveri portal, minimizing paperwork delays.

The critical distinction is between a registered POA and a notarised-only POA.

A notarised POA holds no legal validity for property transactions in India and can lead to title disputes. Registration at the Sub-Registrar’s office is mandatory.

Beyond the POA, most Tier-1 developers now offer virtual site tours, digital documentation, and NRI-dedicated advisory desks that make the remote buying experience practical rather than theoretical.

Myth 2: Indian Real Estate Is Too Risky and Fraud-Prone

The myth: Stories of builder insolvencies, title disputes, and delayed possession have created a widespread perception that real estate investment in India is structurally unsafe, particularly for buyers who can’t monitor construction in person.

The reality:

The Real Estate Regulatory Authority (RERA), established under the RERA Act 2016 and now operational across all states, has changed the legal architecture of Indian property transactions in ways most overseas buyers haven’t fully absorbed.

What RERA mandates that didn’t exist before:

- Developers must maintain 70% of project funds in a dedicated escrow account, ringfenced for that specific project’s construction, preventing the diversion of buyer funds to other projects

- Every project and broker must be separately RERA-registered; buyers can verify both on the state portal before signing anything

- Possession delays attract mandatory interest payments to buyers at the applicable rate

- Buyers have statutory recourse, they can file a complaint via Form M or Form N basis the grievance on the Karnataka RERA portal (rera.karnataka.gov.in) with a ₹1,000 filing fee, and RERA targets resolution within approximately 60 days.

For NRI buyers specifically, RERA provides the same statutory protections as resident buyers. There is no legal distinction in complaint rights or remedies. Verifying tower-wise RERA registration (not just project-level), checking the developer’s complaint history, and confirming the registered completion date on the state portal takes under an hour and eliminates the majority of project delivery risk that once made real estate investment advice for NRIs so cautious.

Myth 3: Returns Are Low Compared to Global Markets

The myth: Indian real estate delivers modest returns that can’t compete with US index funds, Singapore REITs, or other international investment alternatives, particularly once rupee depreciation is factored in.

The reality:

This myth conflates average returns across all Indian real estate with returns in high-growth premium corridors. The rupee depreciation concern is real but requires context.

What the numbers show for Sarjapur Road, Bangalore:

- Property prices rose from approximately ₹6,050 per sq ft at the end of 2021 to over ₹10,800 per sq ft by mid-2025, which is a 79% appreciation over 3.5 years, per Anarock data.

- Gross rental yield in premium IT corridor projects on Sarjapur Road runs 3.5–5.0% annually; premium wellness-oriented developments yield toward 4.5–5.5%.

- Annual capital appreciation of 8–12% in established Bangalore corridors.

The currency depreciation reality check:

The depreciation rate of the Indian Rupee against major currencies is ~3–5% annually, as observed over the past decade. At 10% annual property appreciation and 4% annual depreciation, the net USD-denominated return is approximately 5.8% annually, competitive with international alternatives and carrying the additional option value of a physical asset in a country where many NRIs plan to return eventually.

Consider a 4-year investment scenario:

- Property Purchase: A premium property is bought in Bengaluru for a base price of ₹1.5 crore in 2022.

- Entry Friction Costs: Adding Karnataka’s 5.6% stamp duty and a 1% brokerage fee increases the actual initial capital layout to ₹1.599 crore.

- Property Sale: The asset is sold for a gross price of ₹2.5 crore in 2026.

- Exit Friction Costs: A 1% seller’s brokerage fee brings the realized sale proceeds down to ₹2.475 crore.

- Taxation: A 12.5% Long-Term Capital Gains tax is levied on the net profit of ₹87.6 lakh, resulting in a tax liability of ₹10.95 lakh.

- Net Proceeds: The final net cash in hand after all local taxes and transaction fees is ₹2.365 crore.

- Currency Conversion: Converting the initial capital at the 2022 rate of ₹78/USD requires USD 205,000. Converting the net proceeds at the 2026 exit rate of ₹85.5/USD yields USD 276,660.

- Investment Return: The final net return adjusts from a raw paper gain to a 35% absolute USD return, which equals a 7.8% CAGR in dollar terms.

Thus answering the question: “Is real estate a good investment?” with actual numbers.

Myth 4: Managing Property From Abroad Is Too Complicated

The myth: Tenant disputes, maintenance issues, and the risk of encroachment make it practically impossible to manage Indian real estate from overseas without relying on local family members, or the “trusted relatives trap” that frequently creates its own complications.

The reality:

The combination of professional property management platforms, premium gated-community infrastructure, and properly-structured legal instruments has made genuinely hands-off ownership a realistic option.

What a functional remote management setup looks like:

- Registered POA for leasing and management: scope-limited to tenant agreements and maintenance authorisation, not broad financial authority

- Professional property management services: handle tenant screening, rent collection, routine maintenance, and legal renewals; fees typically run 8–10% of monthly rent.

- Premium gated community selection: projects with dedicated facilities management, 24/7 security, and professional maintenance teams reduce the ad-hoc intervention that low-quality developments require

The single most impactful real estate investment advice for NRIs managing assets remotely is project selection. A well-managed high-rise in a premium development with on-site infrastructure requires dramatically less owner involvement than a mid-rise in an older development with shared borewell and informal maintenance. The quality of the project determines the quality of the management experience, not the owner’s distance.

Myth 5: Only the Rich Can Invest in Indian Real Estate

The myth: Premium Indian real estate, particularly in high-growth corridors like Bangalore’s IT belt, is accessible only to HNIs and ultra-high-net-worth individuals, with entry prices that put it out of reach for most NRI professionals.

The reality:

The mid-premium segment on Sarjapur Road, the corridor with the strongest combination of appreciation, yield, and social infrastructure in Bangalore, starts at approximately ₹1.5 crore for a 3 BHK configuration in IGBC-certified, RERA-approved projects.

For a US-based NRI earning in USD at the current exchange rate of approximately ₹95.65/USD, ₹1.5 crore translates to approximately USD156,815. Against a median US home price of approximately USD 400,000+, a premium Bangalore apartment in a high-growth IT corridor represents a significantly more accessible entry point with higher yield and comparable or superior appreciation in dollar terms.

Home loan financing is also available for NRI buyers: Indian banks and NBFCs offer LTV ratios of up to 80% on NRI home loans, with tenures up to 20 years, and EMI payments can be made from NRE or NRO accounts. At an 80% LTV on a ₹1.5 crore property, the required equity is ₹30 lakh, approximately USD 31,000 at current exchange rates. That is not an exclusively wealthy person’s calculation.

Myth 6: Repatriating Funds Is Difficult

The myth: Once capital is invested in Indian property, getting it back out after a sale is a complex, bureaucratically fraught process that can trap funds in India indefinitely.

The reality:

FEMA provides clear, structured repatriation pathways that are less restrictive than most NRI investors realise:

- If the property was purchased using NRE or FCNR account funds, sale proceeds are fully and freely repatriable with no annual cap, after paying applicable capital gains tax

- If purchased through NRO funds or domestic income, repatriation is capped at USD 1 million per financial year after tax, a limit that covers the proceeds of most residential transactions

- The 2026-27 Union Budget removed the TAN requirement for buyers of NRI properties, replacing it with a PAN-based TDS system, reducing the administrative friction that previously complicated secondary market transactions

The practical process is to pay applicable taxes, file returns, obtain a tax clearance if required, and remit through your Indian NRO/NRE account via normal banking channels. The process involves paperwork but no structural barriers. The perception of funds being “blocked” reflects the old framework, not the current one.

Myth 7: High Taxes Eat All the Returns

The myth: Between TDS deductions at sale, capital gains tax, rental income tax, and municipal property taxes, the effective tax burden on NRI real estate makes net returns negligible.

The reality:

The tax picture is more structured and more manageable than this myth suggests. Here is what the actual liability looks like [VERIFY all figures below against current Income Tax Act 2025 provisions before publishing]:

| Tax Type | Rate | Notes |

| Long-Term Capital Gains (held 24+ months) | 12.5% flat | No indexation; applies to properties purchased on/after July 23, 2024 |

| TDS on NRI property sale (LTCG) | ~14.3% of the sale consideration | Includes surcharge and cess; applies to gross sale value unless Form 128 is obtained |

| Rental income TDS | ~31.2% | Tenant must deduct from gross rent; no threshold limit applies. |

| BBMP property tax | 0.1% of Guidance Value | Self-occupied rate; changes to 0.2% if property is rented. |

The tools that reduce effective tax:

- Form 128 (Lower TDS Certificate): Formerly Form 13, this allows the NRI seller to apply for tax deduction only on actual capital gains rather than the gross sale value which is a significant liquidity difference. On a ₹1.5 crore sale with ₹50 lakh of actual gain, TDS on gains (₹6.25 lakh) vs. TDS on gross value (₹21.45 lakh) represents a difference of over ₹15 lakh in immediate cash flow

- Section 54 reinvestment exemption: Reinvesting capital gains into another residential property within the statutory timeline exempts those gains from LTCG tax entirely

- DTAA relief: India has Double Taxation Avoidance Agreements with over 90 countries. NRIs can claim credit for taxes paid in India against their home country tax liability, preventing the same income from being taxed twice

The tax framework has friction, but it has structure; and that structure provides tools that any well-advised NRI buyer can use to manage effective liability meaningfully below the headline rates.

If these myths have kept you from investing back home, explore how Suyug makes NRI buying straightforward with RERA-approved projects on Sarjapur Road, IGBC-certified, designed for buyers who need an asset that works reliably from a distance.

One Thing Worth Sitting With

The myths that hold NRI investors back from real estate investment in India are not invented. They have roots in real experiences from a decade ago. What has changed is the regulatory framework, the quality of premium supply, and the transparency infrastructure around it. The question for a buyer in 2026 is not whether Indian real estate is safe. It’s whether the specific project, developer, and sub-location they’re evaluating can pass the verification steps made possible by the new framework. That answer is findable, and it usually takes less time than the hesitation does.

FAQ’s :

Yes, via a registered Power of Attorney (POA) attested at your nearest Indian Embassy and adjudicated at the Sub-Registrar’s office in India. The POA should be transaction-specific, and not general, to limit risk. Most Tier-1 developers now offer virtual tours and digital documentation for the full process.

RERA mandates that 70% of buyer funds are held in project-specific escrow, requires separate registration for every project and broker, and gives buyers statutory recourse for delays via an online complaint portal. For NRIs, the protections are identical to those of resident buyers. Verifying RERA registration tower-wise on rera.karnataka.gov.in takes under an hour and significantly reduces delivery risk.

In Bangalore’s premium IT corridors, annual appreciation of 8–12%, combined with rental yield of 3.5–5.5%, gives USD-denominated returns that are competitive with international alternatives after accounting for rupee depreciation. Indian real estate also carries option value, that is, the eventual ability to use the asset personally — that purely financial instruments don’t. The comparison is most favourable in high-growth micro-markets with confirmed infrastructure tailwinds.

For properties held over 24 months, LTCG is taxed at 12.5% flat without indexation (for assets purchased on/after July 23, 2024). The TDS applied at sale runs approximately 14.3% of gross sale consideration. However, applying for Form 128 (Lower TDS Certificate) before the sale reduces this to tax on actual gains only, which can represent a significant cash flow improvement. Section 54 reinvestment exemptions can eliminate LTCG tax entirely, if gains are reinvested in residential property within the statutory timeline.

Properties purchased with NRE or FCNR funds: sale proceeds are fully repatriable after tax, with no annual cap.

Properties purchased through NRO funds: repatriation is capped at USD 1 million per financial year after paying applicable taxes.

The 2026-27 Budget’s removal of the TAN requirement has reduced administrative friction in secondary market transactions, making the process more straightforward than it has historically been.

In Sarjapur Road’s mid-premium segment of IGBC-certified, RERA-approved, no-shared-wall projects from established developers, the entry prices for 3 BHK configurations start at approximately ₹1.5 crore. At a rate of approximately ₹95.65/USD, that’s roughly USD 156,815, which is accessible via NRI home loans at LTV ratios up to 80%, requiring an equity contribution of approximately ₹30 lakh (around USD 31,364). The total acquisition cost, including stamp duty, registration, and GST, comes to approximately 15–18% above the base price.